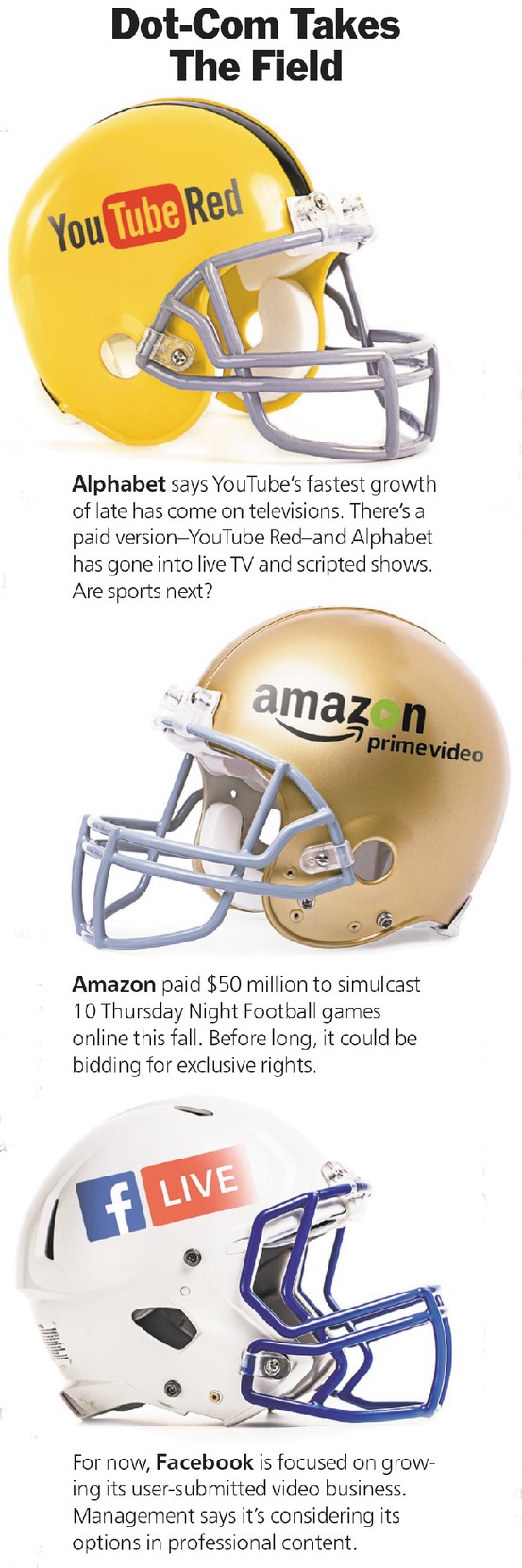

Are you ready for some football? Amazon.com is. A few months ago, it agreed to pay the National Football League $50 million for streaming rights to 10 Thursday Night Football games starting on Sep. 28. That’s five times what Twitter paid for a similar deal last season.

For now, streaming is a mere sideshow to television in sports. The Thursday games will air simultaneously on the NFL Network, and on either CBS or NBC, which each pays $225 million a year for five of them. But Amazon’s encroachment should give media investors pause. Viewership trends in television are weak, and they’re worse without sports. Whereas TV networks own many of their scripted hits, they rent sports. Wisely, they have locked up rights for years to come, albeit at rich prices. As those rights come due, the networks could enter an unwinnable bidding war with Amazon (ticker: AMZN),Facebook (FB), and Alphabet (GOOGL).

“Winter is coming,” says New York University marketing professor Scott Galloway, borrowing a grim refrain from the HBO hit Game of Thrones. “The post-sports world will be ugly for television.”

Winter might already be here for cable networks that lack the programming might of the broadcast bigs. Last Monday, Discovery Communications (DISCA), which owns the Discovery Channel and TLC networks, said it will buy HGTV and Food Network ownerScripps Networks Interactive (SNI) for $11.9 billion. Both companies also reported disappointing financial results amid subscriber declines. “This deal combined with [second quarter] results suggests how tough the cable network business has become,” wrote Wells Fargo Securities analyst Marci Ryvicker. In a presentation, Discovery touted the combined company’s potential for cost savings and overseas expansion. But its shares finished the week down 11%, capping a 25% slide over two years. Scripps shareholders are getting a deal premium exceeding 30%.

Scripps and Discovery aren’t the only cable network operators facing challenges.Viacom (VIAB), the owner of MTV, Comedy Central, and Paramount Pictures, beat earnings estimates, but reported a 2% dip in domestic ad revenue. Skittish investors pushed the shares down 14% Friday in response.

FOR NOW, the major broadcast networks—CBS (CBS); ABC, owned by Walt Disney(DIS); NBC, owned by Comcast (CMCSA); and Fox, owned by Twenty-First Century Fox (FOX)—are better positioned than cable. (Twenty-First Century Fox and News Corp (NWSA), publisher of Barron’s, shared common ownership until 2013.) As must-carry channels, they have negotiated for rising fees from cable operators, while raising prices for advertising, which is helping to offset declines in cable subscribers and ratings.

All have large in-house production operations that can create shows for the new crop of online streaming services. Some have fee-based streaming platforms of their own, or plans to launch them. Others are part of media conglomerates with a hand in theme parks, cable-TV distribution, and more. But the protective moat of the cable bundle is already weakening, and sports rights could be next. Before that happens, valuations for the group could come down to reflect the rising risk.

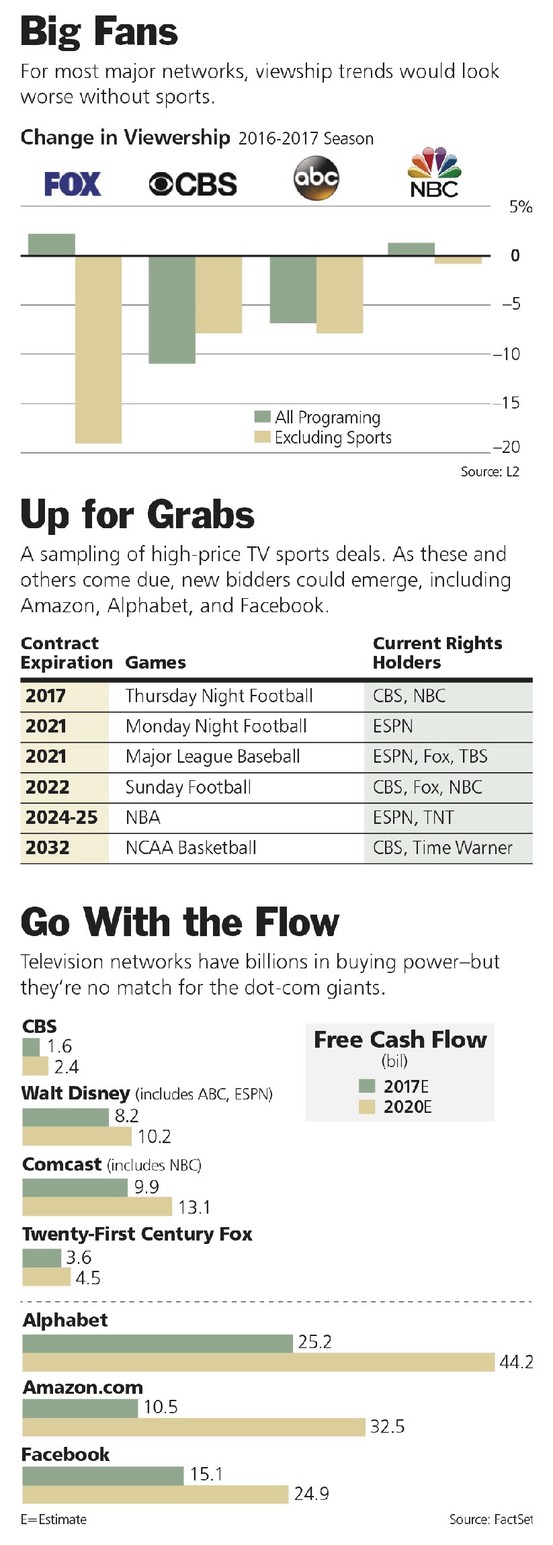

Sports are the biggest draw on television. Among last year’s 50 most-watched telecasts, 44 were football, basketball, baseball, or the Olympics. Sports viewers are also particularly attractive to advertisers. They skew young, and thus have plenty of years ahead to spend on their favorite brands, and they like to watch games live, which means they catch more commercials instead of zipping through them on their digital video recorders. TV networks have increased the number of hours devoted to sports by 160% since 2005.

At the same time, traditional television is losing its reach. Over the past five years, viewership among teens and young millennials (ages 18 to 24), including delayed viewing on DVRs, but not online streaming, has plummeted by more than 40%, according to Nielsen data. Among older millennials (25 to 34) and Gen Xers (35 to 49), it is down 28% and 13%, respectively. Only over-50s are sticking with their clickers.

Some of those lost younger viewers are watching traditional TV shows on new platforms, including smartphone apps for shows, networks, and cable carriers. But many are spending their screen time with services like Netflix (NFLX), which now boasts more U.S. subscribers than all cable carriers combined. If TV networks are struggling to remain relevant, TV sets are not. As of March, according to Nielsen, 23% of U.S. households had an Amazon Fire TV, Apple TV, Chromecast, or Roku device for streaming movies and shows through their televisions, up from 19% in June 2016. Another 11% of households stream to their TVs using other devices, including smartphones and tablets; 29% own TVs with built-in apps for streaming; and 42% have videogame consoles that double as TV streaming devices.

Across these devices, streaming apps are proliferating. Apple (AAPL) says it will add Amazon Prime Video service to Apple TV this year, while Facebook (FB) is working on a video app for Apple and Amazon devices.

SPORTS HAVE NOT BEEN IMMUNE to viewership declines, although one man has made recent trends difficult to read: Donald Trump. Football ratings tumbled leading up to Election Day, but stabilized afterward. Basketball ratings fell long after Election Day, although they were even with their level two years ago. Baseball was solid. Trump’s antics seem to have made news more intriguing than sports at times, with the notable exception of the Chicago Cubs winning their first World Series in more than a century.

There were other factors at play.

Football, for example, faced controversies over a string of player protests during the singing of the national anthem, and over mounting evidence that the game causes brain injuries. One thing is certain: TV viewership would be much lower without sports. For most of the major networks, it would be declining faster, too, according to NYU’s Galloway (see chart, “Big Fans”). A spokesman for Nielsen declined to comment.

Nielsen has been working to add new ways of measuring audiences across traditional and digital platforms, including YouTube and Hulu, but for now, ratings are a source of frequent dispute. According to a unit of the Interpublic Group of Companies, a collection of advertising concerns, overall television ratings have fallen 33% in four years, while ad prices have climbed 20%. Some networks call statements like that an effort to negotiate advertising tabs lower.

TV HAS FACED spiraling costs for sports rights for decades. Upstart Fox bid aggressively for games in the 1990s to help secure its place as one of the major networks. ESPN, easily the most expensive channel in typical cable bundles, at more than $7 a month per subscriber, has used its rising financial might to secure a growing slate of professional games. Sports pundits say it overpays for programming, relative to the major networks, but Disney has said it is happy with its contracts.

For some sports, and some particular games, TV has paid dearly to protect its rights for many years. ESPN and Time Warner’s TNT hold National Basketball Association rights that extend through 2025 under a combined $25 billion, nine-year deal. CBS and Time Warner (TWX) are together paying $10.8 billion for “March Madness” college basketball games through 2024, plus another $8.8 billion to extend through 2032. Other deals are shorter. CBS, Fox, and NBC have Sunday football games through 2022 under a nine-year deal that costs $27.9 billion combined. Thursday night games are up for bid after the coming season.

Such high prices have led investors to wonder whether TV rights for sports are a bubble waiting to pop. The average cable subscriber now pays more than $20 a month for sports. Not everyone watches sports, of course, which is part of the reason subscribers have been cancelling service. RBC Capital Markets estimates that cable’s subscriber base will decline by 3% this year, which would be about twice the rate of decline seen last year.

TV’S SPORTS PROBLEM amounts to this: If last year’s disappointing viewership is the start of a secular decline—because viewers are too busy, or the games or seasons are too long, or the entertainment alternatives are better, or what have you—then TV has bet big, right at the top of the market. On the other hand, if sports fans stay as glued to their games as ever, TV could soon have to compete with a crop of new rights bidders on financial steroids.

Alphabet, which owns YouTube and Google, and Facebook, which owns Instagram, are a mirror image of broadcast TV. Their audiences are vast and growing. Consider: Various Super Bowls dominate the list of the most-watched U.S. telecasts ever. But there are more than 40 YouTube videos that have each been watched 10 times more than any Super Bowl. Advertisers are quickly shifting dollars online. Digital ad spending passed advertising outlays for TV for the first time last year. This year, the gap will widen to $10 billion—with $83 billion for digital, and $73 billion for TV, according to industry forecaster eMarketer. By 2021, the gap could be more than $50 billion. And while TV is in a spending race for content, YouTube and Facebook get free content created by their users.

Meanwhile, Amazon seems to be trying—and failing—to spend money as fast at it makes it. This year, it is likely to generate $10.5 billion in free cash, more than any television network’s parent company. And Amazon’s free cash flow could triple by 2020. By then, Wall Street predicts, the big four TV networks and their parent companies—with their theme parks, movies, and other ventures—will generate a combined $30 billion in free cash flow. Alphabet, Facebook, and Amazon are seen combining for more than $100 billion.

ALL THREE DOT-COMS have a strong and growing interest in video. Amazon offers a subscription video service as a giveaway to customers who pay $10.99 a month, or $99 a year, for its Amazon Prime shopping service with free two-day shipping—but that giveaway service won three Oscars this year. Alphabet says that YouTube viewing time on televisions has nearly doubled over the past year. It has a fledgling subscription service called YouTube Red and a new live TV package called YouTube TV. Last quarter, it unveiled six new original shows with stars such as Ellen DeGeneres and Kevin Hart.

Facebook on its latest earnings call touted video as a growth and investment priority. “Video is the most engaging experience that we can offer,” said finance chief David Wehner. User videos are the core focus for now, but “there’s opportunities for semiprofessional and professional content,” he said.

If Netflix has gotten limited mention here, it is only because its popularity in streaming greatly exceeds its spending power for now. The company isn’t expected to generate positive free cash flow for at least five years.

There is much more to producing sports on TV than simply paying for rights. The Emmys have 41 categories for sports, including play-by-play, studio host, camera work, and audio. Local-market and advertising expertise matters, too. But scripted programming is complicated, and the streamers seem to have gotten the hang of that, judging by their growth rates. All of this means that media investors should take care to favor only companies that look capable of managing a future sports cliff.

Comcast has the strongest hand of the bunch. It owns the only major cable carrier that has added video subscribers of late. The carriers, in general, are well positioned to deal with cord-cutting, because it’s something of a misnomer. Customers do without their video signals, but they become all the more dependant on the cords that bring their broadband internet service. Cable carriers take advantage of this by bumping up the price on broadband for subscribers who cancel their video. As a result, Comcast can prosper for years to come, regardless of who wins the war for viewers. Meanwhile, theme park profits are galloping higher after years of spending on expansions.

CBS IS MUCH CLOSER to being a show-business pure play, but it has led in television ratings for years, which helps when the company pitches cable carriers for higher fees. The company also has streaming services of its own in Showtime Anytime and CBS All Access. The valuation is attractive. Whereas Comcast sells for close to 20 times this year’s earnings forecast, CBS goes for less than 15 times. Wall Street predicts 16% earnings-per-share growth next year, but estimates have been gradually coming down. We recommended the stock in a cover story a year ago (“Will CBS Buy Viacom?” Sept. 24). It has returned 26% since then, compared with 16% for the Standard & Poor’s 500 index.

Disney has heavy sports exposure through ESPN, the company’s biggest earner. But it also owns a flourishing theme-park business and has one of the best win records in the movie business in recent years. All of that is worth a premium price, but the stock already carries one, at 18 times projected earnings for calendar 2017, and earnings growth has recently slowed. Disney has plans for a streaming service for ESPN that will bypass cable, and has a stake in Major League Baseball’s streaming arm, BAMTech.

Fox’s CEO, James Murdoch, has told analysts that the company could offer a direct-to-customer model in the future. For now, Fox, like Comcast, Disney, and Time Warner, has a stake in the streaming service Hulu. By 2020, predicts eMarketer, Hulu will have 35.8 million subscribers, behind Amazon Prime Video, with 96.5 million and Netflix, with 139 million.